One of the worst experiences for a homeowner is filing a home insurance claim only to be told it’s not covered. After years of paying premiums, the insurance company doesn’t deliver when it’s needed most. What a disappointment.

This disconnect happens because we rarely take the time to review our home insurance policies each year. With confusing terms like Actual Cash Value (ACV) and Replacement Cost Value (RCV), it’s easy to feel overwhelmed and ignore the details.

But as a Financial Samurai, it’s crucial to always be prepared for the worst. Whether it’s knowing how to protect your family from a home invasion, spotting a staged car collision scam, or anticipating the policies your next mayor might push, being prepared empowers you to keep moving forward, no matter the challenge.

A Review Of Your Home Insurance Policy

Let’s review some home insurance basics. If you have a mortgage, your bank requires you to carry insurance, which you pay for. However, if you own your home outright, you’re not legally obligated to maintain coverage.

Below is an example snapshot of a home insurance policy costing $3,900 a year, and I’ll walk through each item.

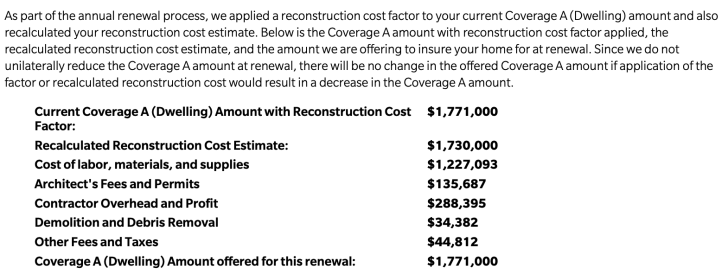

Dwelling Coverage (Coverage A, $1,771,000)

Dwelling coverage is the amount needed to repair or rebuild your home. In this example, the dwelling coverage is $1,771,000 for a 4,800 square foot home, which translates to $369 per square foot. It’s important to do this calculation and compare it to the current cost of construction in your area.

In San Francisco, $369 per square foot is low, but it’s likely more than sufficient in places like Little Rock, Arkansas. According to Farmer’s Insurance, the industry standard is closer to $602 per square foot in San Francisco. Ask your home insurance agent what your city’s standard is.

If you live in an area where property values and construction costs are rising, your dwelling coverage may gradually become insufficient. Some insurance companies automatically adjust your coverage every few years, but in many cases, you’ll need to proactively ensure your coverage amount is accurate.

Below is a breakdown of how they arrived at the $1,771,000 in dwelling coverage. This breakdown also gives insights on the high cost of remodeling an undamaged home.

Personal Property (Coverage C, $708,400)

Personal property insurance covers your belongings—furniture, electronics, appliances, clothing, and anything else that would fall out of your house if you turned it upside down. In this example, personal property coverage is $708,400, which is 40% of the dwelling coverage. That’s a substantial amount! Many policies set personal property coverage as a percentage of dwelling coverage, often with 40% being the minimum.

This approach offers an interesting glimpse into U.S. consumer culture. Insurance companies base these percentages on millions of past claims to establish a baseline.

Personally, I find $708,400 excessive for my belongings. Aside from collectibles (coins, books, sports memorabilia) and family pictures, there isn’t much of significant value in my home. We don’t own designer furniture or expensive art. So, if a robber targeted my house, they’d be disappointed.

For those following a minimalist lifestyle, like many personal finance frugal enthusiasts, this coverage might feel far too high.

Separate Structures (Coverage B, $88,550)

This covers the cost of repairing or rebuilding structures on your property other than your main home, such as fences, a barn, or a detached garage. It’s important to clarify with your agent whether an attached garage without living space counts as a separate structure. In most cases, it should be considered part of the main dwelling.

Personal Liability (Coverage E, $300,000)

Personal liability coverage protects you if someone is injured on your property or if you’re legally responsible for damages to another person’s property. Here are some examples of what it might cover:

- A guest falls down your stairs

- Your child breaks a neighbor’s vase

- A delivery person slips on your sidewalk and breaks their arm

- Your dog bites a neighbor

- A tree falls and damages a neighbor’s property

For those who entertain frequently at home, personal liability coverage is crucial. In this example, the policy includes $300,000 in liability coverage, which seems reasonable. However, if you host a large party and your balcony collapses, that $300,000 could be quickly exhausted.

Loss of Use Coverage (Coverage D, $177,100)

Loss of use coverage is essential because you’ll need a place to live if your home becomes uninhabitable. Depending on your location, it could take years to get permits and rebuild.

To calculate your needs, estimate the monthly rent for a comparable home, multiply by how long you think the rebuild will take, and then add 50% as construction often takes longer than expected.

For example, if renting a similar home costs $5,000 per month and you anticipate a 12-month rebuild, multiply $5,000 by 18 months to get $90,000. For total destruction, plan on 24-30 months of renting elsewhere.

In this home insurance policy, Coverage D accounts for 10% of Dwelling Coverage.

Medical Payments (Coverage F, $1,000)

Medical payments coverage takes care of reasonable medical expenses for guests accidentally injured on your property. It can cover medical bills, ambulance rides, stitches, X-rays, and more. This coverage is designed to offer a quick resolution to minor injuries, avoid lawsuits, and show goodwill. It doesn’t apply to you, your household members, or injuries related to business activities.

The maximum limit is typically $5,000, but you can often increase it. In this example, medical payments coverage is only $1,000, which you may want to increase.

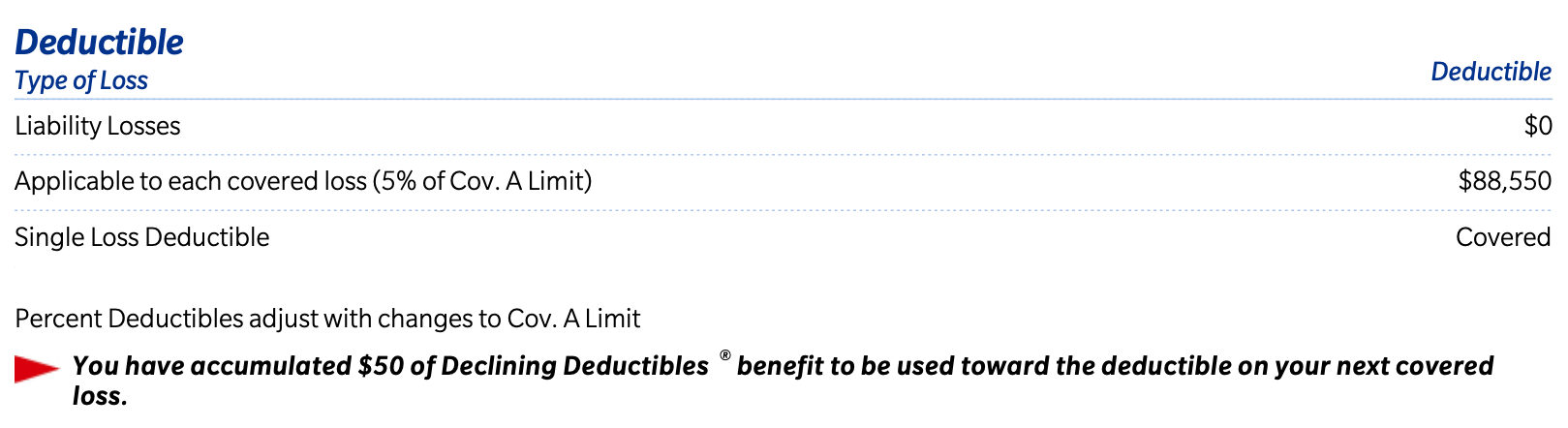

Home Insurance Deductibles – Important To Know!

A homeowner must pay a deductible before the insurance company pays out a claim. Deductibles are usually 1% to 10% of your dwelling coverage (Coverage A). The higher the deductible, the lower your premiums, and vice versa.

Let’s review the deductible for this policy.

Liability coverage (Coverage E) with a $0 deductible means you don’t pay out of pocket for liability claims. For example, if someone slips and falls on your property and sues you, the policy will cover up to $300,000 without any deductible. The insurance pays the claim up to the coverage limit stated in the policy.

This home insurance policy has a deductible of $88,550 for each claim under Dwelling Coverage (Coverage A). If you experience a loss, it must exceed $88,550 for coverage to apply. For instance, if a fire causes $120,000 in damages, the insurance will cover $31,450, while you pay the first $88,550.

Important Action Point on Deductibles

Insurance carriers often set a default deductible when quoting a policy. It’s essential to ask how the premium changes at different deductible levels, ranging from 1% to 10% of your Dwelling Coverage. Your goal is to find the right coverage at the right cost.

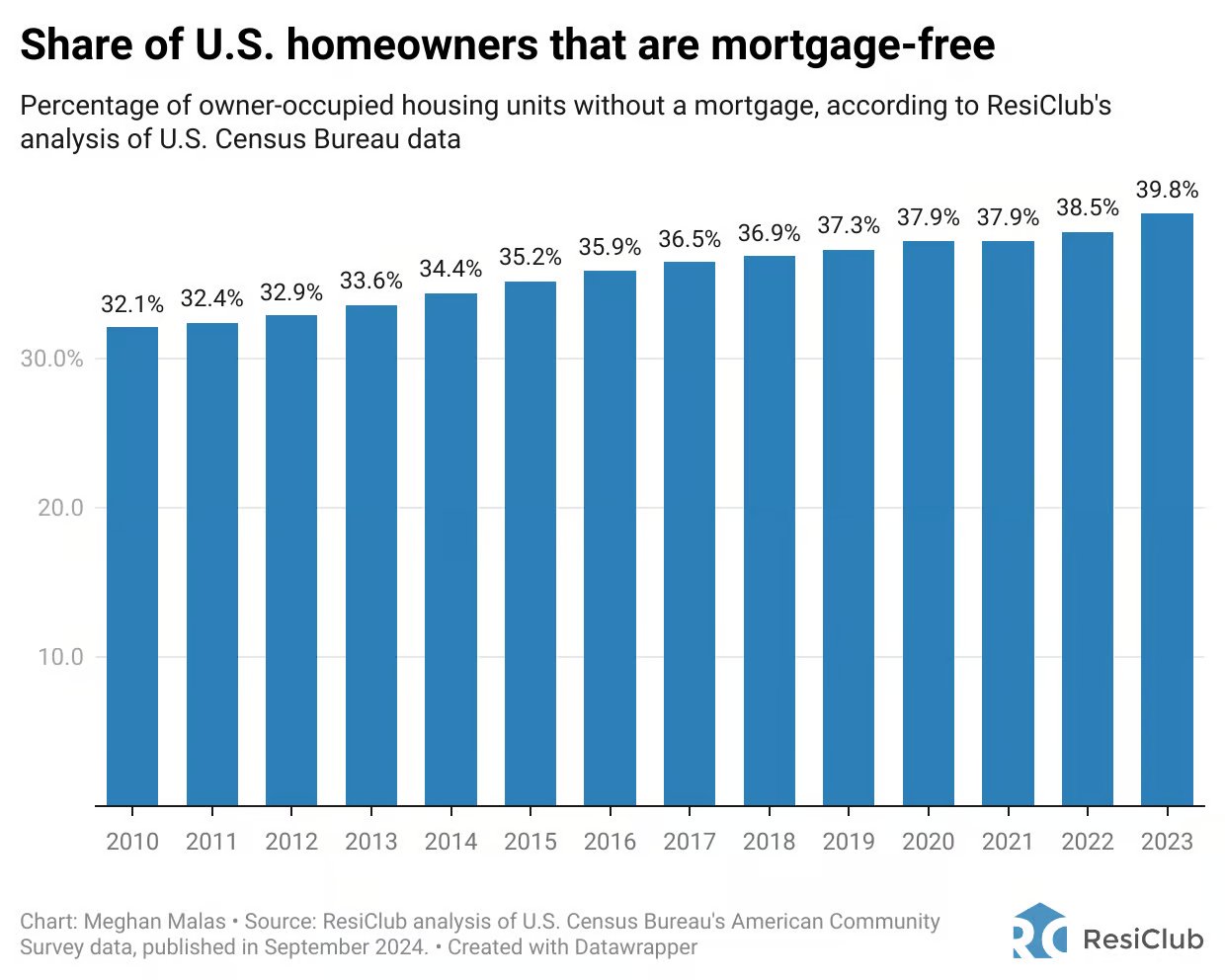

For example, if you’re among the 40% of homeowners in America without a mortgage, and your primary residence makes up only 20% of your net worth, you might not need extensive coverage. You could raise your deductible to 10% of Dwelling Coverage, which in this case would be $177,100. Doing so might reduce your premium from $3,900 to $2,900. The decision comes down to whether saving $1,000 annually is worth the higher out-of-pocket cost for claims.

Opting for a high deductible essentially provides you with catastrophe coverage. If you live in an area with no history of frequent catastrophes, this could be a worthwhile strategy. However, if your region experiences regular disasters, you might prefer a lower deductible despite the higher premium.

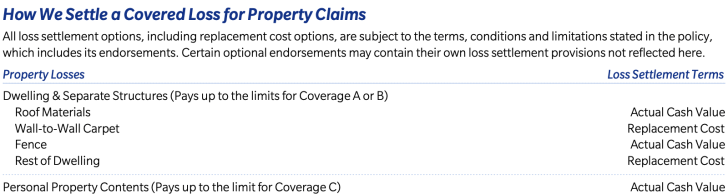

Actual Cash Value vs. Replacement Cost

When settling property claims, it’s critical to understand the difference between Actual Cash Value and Replacement Cost. When filing a claim, Replacement Cost is preferable, as the insurance company covers the current cost to replace damaged items. In contrast, Actual Cash Value takes depreciation into account, meaning you may receive far less.

For example, this policy pays ACV for roof materials. If your roof is 40 years old, the insurance company might only pay 10% of the cost to replace it, while Replacement Cost coverage would pay 100%.

According to Farmer’s Insurance, if they lack records showing the roof was replaced within the last 15 years, the policy defaults to ACV, which can also apply to fences and other structures—ultimately saving the insurer money while costing the homeowner.

Of course, Replacement Cost coverage is more expensive than Actual Cash Value. That’s why it’s important to ask about the cost difference. If you’ve recently remodeled your home or replaced the roof, opting for Actual Cash Value coverage could save you money.

But if your home is 60 years old, Replacement Cost coverage might be worth the extra expense. It’s like getting a new iPhone 16 to replace your damaged iPhone 7 with Replacement Cost.

The Most Common Home Insurance Claims in California

Now that you know all the home insurance coverage basics, I thought it’d be good to share the most common home insurance claims in California. The percentages will vary by state to state, but at least these percentages will give you a good idea for optimal coverage and protection.

- Water damage: The most frequent claim, making up 56.9% of all homeowners insurance claims. Of these, 17.44% are due to plumbing leaks within walls or shower pans.

- Wind and hail damage: These account for nearly 16% of claims, including damage from falling trees, flying debris, and harm to fences, roofs, and homes.

- Other covered losses: Represent 10.25% of claims and include equipment breakdown, spoilage, service line damage, and walls or fences hit by vehicles.

- Theft and break-ins: Make up 9.41% of claims.

- Fires: Comprise 4.03% of claims, often resulting in significant damage from lightning or kitchen fires.

- Bodily injury: The least common, accounting for 1.16% of claims.

If you’re remodeling or building a house, pay close attention to the plumbing. Pipes erode and joints fail. If your plumbing hasn’t been updated in decades, it’s wise to consider some preventative maintenance. In my experience, water damage has been the most common issue by far. I’ve had repair a ceiling due to a flooded tub, fix a broken water, reinstall leaking windows, and repair a leaking light well.

Looking back at the water damage incidents in my homes over the past 21 years, I wouldn’t have filed an insurance claim for any of them. Each repair cost less than the deductible.

The Growing Cost Of Home Insurance

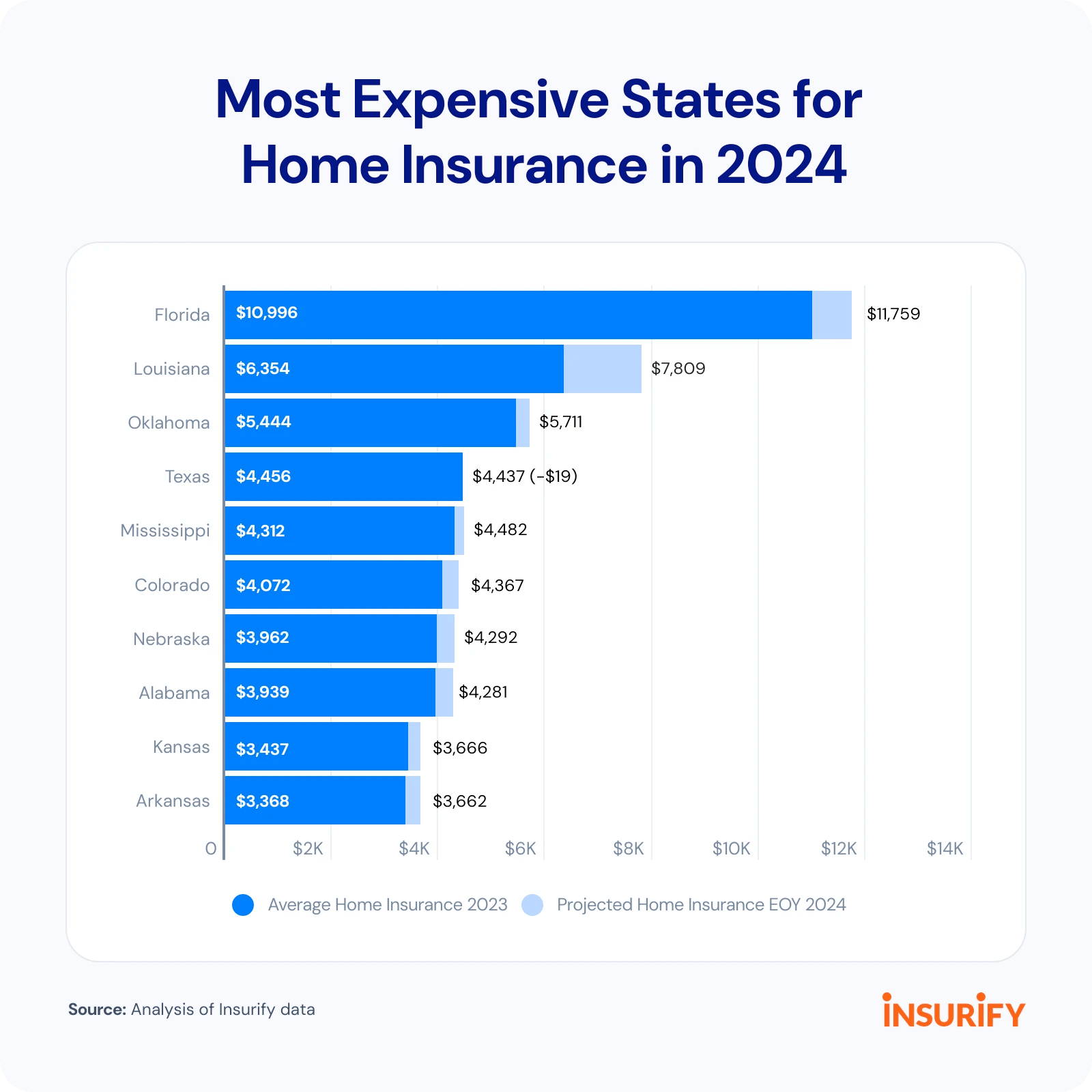

Home insurance costs are rising due to several factors: natural disasters, increasing construction costs, more people moving to high-risk areas, and industry consolidation. Nationwide, premiums rose by 34% between 2017 and 2023, and they continue to climb.

Below are the most expensive states for home insurance in 2024, with Florida leading at about 3.5 times the national average. Surprisingly, California isn’t in the top 10 despite the attention it receives for wildfires. This is because fire risks are concentrated in specific regions, such as Sonoma and Napa counties.

If you’re planning to buy a home, it’s crucial to get a home insurance quote beforehand. This will give you a clearer picture of your total cost of homeownership. Just like the true cost of owning a car includes maintenance, taxes, insurance, and potential tickets, the true cost of owning a home extends beyond the purchase price.

Know Your Home Insurance Policy Inside And Out

I hope this gives you a clear overview of what to look for in a home insurance policy. If you’re ever unsure about a term or a specific situation, don’t hesitate to ask your insurance agent. Come up with various home insurance claim scenarios and have them explain how much you would pay versus how much the insurance company would cover.

Your goal is to find the most affordable policy that adequately protects one of your largest assets. A key part of feeling secure is understanding exactly what your home insurance policy covers—and what it doesn’t.

Stay safe and knowledgeable, everyone!

Have you reviewed your home insurance policy recently? If so, did you update any coverage amounts? What are your thoughts on choosing a lower deductible versus a higher deductible? And would you consider going without home insurance once your mortgage is paid off?

Invest in Real Estate Without the Hassle

Real estate is my favorite asset class for building wealth. If you want to invest in real estate without dealing with tenants, maintenance issues, or insurance agents, check out Fundrise.

Founded in 2012, Fundrise manages over $3.3 billion for nearly 400,000 investors. The firm focuses on single-family and multi-family properties in the Sunbelt, where property valuations are lower and cap rates are higher. With the Federal Reserve likely to enter a multi-year rate cut cycle, the potential for lower mortgage rates could boost demand.

I’ve been investing in private real estate since 2016 to diversify my portfolio and generate more passive income. Fundrise has been a long-time sponsor of Financial Samurai, and I’ve personally invested over $270,000 in Fundrise to date.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009.

Read the full article here