The retirement crisis: How did we get here?

Despite modest improvements in the retirement savings landscape, millions of Americans remain dangerously underprepared for their golden years. With 28% of people having no retirement savings and nearly a third of working Americans holding less than $1,000, the reality is clear: financial insecurity is looming large, especially for older adults on the brink of retirement.

Retirement in America is in crisis

As of 2024, the state of retirement savings in the U.S. has shown some improvement—if you squint hard enough. But let’s be real: many Americans are still tiptoeing toward their golden years with empty pockets. According to a recent Yahoo Finance report, 28% of Americans have precisely $0 saved for retirement. That’s right—zilch, nada, not even a rainy-day penny under the mattress. Meanwhile, 30% of working folks have managed to scrape together a whopping $1,000 or less, which might get them through a luxurious weekend of ramen and Netflix.

And it gets worse. Among people aged 65 and older—the very demographic that should be kicking back with a piña colada on some tropical beach—about 14% have saved less than $1,000 for their entire retirement. If you thought Social Security was going to swoop in and save the day, grab that cup of ramen because it will be a long ride.

Now, while some of these numbers may have improved slightly since the last decade, the reality is that many Americans are still woefully unprepared for retirement. 46% of households at least have some savings squirreled away, but let’s not break out the champagne just yet. The gap between those who are prepared to retire in comfort and those who will struggle to make ends meet is widening as healthcare costs rise faster than Beyoncé ticket prices.

So, what’s going on? Why can’t Americans save for retirement?

Are Americans financially reckless? Absolutely not. Most people are smart enough to know that, unless they plan to live off their cousin’s couch, they’ll need some cash when they stop working. The problem, as always, is more nuanced than that.

It’s likely one of two things, or both: Americans simply can’t afford to save or are too caught up in today’s expenses to focus on tomorrow’s needs. And let’s be honest, with inflation turning grocery shopping into a game of “What can I live without?” it’s no wonder people are choosing to live in the present. It’s hard to think about your 75-year-old self when your 35-year-old self is stressing over this month’s rent and that student loan bill you’ve been side-eyeing for years.

Yahoo Finances’ and other findings aren’t exactly earth-shattering—after all, we’ve been hearing the same tune for years. Every few months, a new university or think tank study reminds us that Americans are falling behind on retirement savings. And while it’s tempting to believe that people are just ignoring the warnings, the truth is much more complex. Between stagnant wages, the high cost of living, and the unpredictable economy, saving for retirement feels less like a prudent financial goal and more like wishful thinking.

It’s not that Americans don’t want to save for retirement. Most do. However, whether due to immediate financial pressures, the simple fact that tomorrow feels very far away (see hyperbolic discounting), or that wages have been virtually stagnant since the 1970s, many people just can’t prioritize it.

Americans can’t save for retirement

One of the most plausible reasons Americans aren’t saving enough for retirement is that they simply can’t afford to.

The average American wage, particularly for middle- and lower-income earners, has remained largely stagnant since the 1970s. While it may seem like wages have gone up at first glance, the devil is in the details. For instance, the median household income in 1984 was $22,415; by 2014, it had risen to $53,891—a 140% increase. But here’s where things get tricky: inflation, skyrocketing living costs, and the fact that more households rely on dual incomes muddy that seemingly positive statistic.

The 2-income trap

In 1984, 60% of mothers with children under 18 were in the workforce; by 2012, that number had jumped to 71%. More earners in the house should mean more money to go around, right? In theory, yes. The increased cost of living has devoured these dual incomes like a hungry teenager at an all-you-can-eat buffet. This isn’t to shame working moms or households where both parents work. It’s just the financial effect of the culture change.

Housing costs: A towering obstacle

Consider the cost of housing. In July 1984, the median price for a new home was $80,700 per the US Census. Fast forward to today, and that price has ballooned by 431%, with the median home now costing $428,096, according to Redfin. For many, buying a home has become less of a rite of passage and more of an Olympic sport, with the finish line always just out of reach.

The cost of just getting around

Then there’s the cost of transportation. According to the Chicago Tribune, in 1984, owning a car cost about $5,000 a year. AAA says today’s cost has surged to $9,282 annually—an 86% increase. So, while your car may now come with heated seats and a backup camera, it’s also burning a bigger hole in your wallet.

College costs: They’ll make you cry

Education is another area where costs have gone off the rails. Sending a student to a four-year public college in-state costs around $24,513 annually per U.S. News & World Report. That’s a 437% increase from $4,563 (National Center for Education & Statistics) in 1984, when it was a much more digestible figure. That’s enough to make anyone reconsider those extra courses in underwater basket weaving.

Healthcare or medical debt scare?

The real kicker, though, is healthcare costs. In 1984, according to the National Institute of Health, most families paid a modest $1,580 yearly for their health insurance. Today? Families are forking $7,620 annually, per Forbes – a 382% increase. And that’s before you even get to the co-pays, deductibles, and random bills for “facility fees” (whatever those are).

Eggs: Even chickens are charging more

Here’s a contentious topic during the Trump/COVID/Biden/Harris era. Even the cost of everyday staples has spiked. Eggs cost about $1.30 per dozen in 1984. Today, per SoFi, eggs are averaging $3.00—a 131% increase. Sure, that might not seem like much, but every penny counts when you’re cracking eggs into your retirement plans.

The Bigger Picture: Americans Are Drowning in Costs

These figures paint a pretty clear picture: the cost of living has far outpaced wage growth. For many Americans, the dream of retirement savings is less of a “pipe dream” and more of a luxury only a few can afford. Between housing, healthcare, transportation, and everyday necessities, the average American is just trying to keep their head above water, let alone build a retirement fund.

In a world where 46% of Americans have some savings for retirement (USA Facts), the gap between those who can and those who can’t save for their future is growing. So, the next time someone says, “Why don’t Americans just save more for retirement?” feel free to toss out these numbers, along with a side of expensive eggs, for a little perspective.

American’s carpe diem thinking

Another reason many Americans may be sidelining their retirement plans is that they are too caught up in the pleasures and demands of the present. After all, when the allure of immediate gratification is this strong, who wants to think about something as distant and unexciting as retirement? Americans are spending more than ever on necessities and luxuries we now view as essentials.

A snapshot of spending habits

Take a look at some eye-popping stats:

- Home sizes have ballooned, with the average home size increasing from 1,605 square feet in 1984 to 2,140 square feet in 2024, per the U.S. Census Bureau. Every American now needs an extra 1,000 square feet to store all the stuff we’re buying.

- The cost of watching TV has also exploded. Today’s families are shelling out anywhere from $90 to $120 per month for TV, streaming, and internet bundles, compared to my dad’s grumbling about his $12 cable bill back in the day, including HBO; thank you very much! Now, HBO alone will set you back around $10 – $20 a month.

- Then there’s eating out. A plurality of Americans now eat out at restaurants once a week or more (Statista.com). That’s a lot of Taco Tuesdays, which may explain why saving for future Taco Tuesdays in retirement seems less of a priority.

The price of convenience and luxury

What do these trends tell us? The cost of just about everything we “need” or think we need has skyrocketed. And it’s not just the obvious big-ticket items like housing and cars. Consider all the modern “essentials” we didn’t even have in 1984—smartphones, high-speed internet, personal computers, and the dreaded $8 daily coffee habit. These are now considered non-negotiable staples of daily life. Add in the constant pressure to upgrade, refresh, and stay trendy, and it’s no wonder people are more focused on financing today than worrying about tomorrow.

In a sense, many Americans are playing the role of the grasshopper from Aesop’s fable, living it up today and figuring they’ll deal with winter (retirement) when it comes. After all, “Why bother about winter? We have plenty of food at present,” as the grasshopper famously said before learning the hard way that winter waits for no one.

A million bucks isn’t enough anymore

To make matters worse, even those who manage to scrape together a nest egg may find that $1 million in retirement savings—once seen as a surefire ticket to comfort—is now barely enough to maintain a middle-class lifestyle for 20 or 30 years. With inflation chipping away at the value of every dollar, retirees today need more than ever just to cover the basics, let alone live the “fabulous retirement” they’ve been dreaming of.

Why retirement insecurity isn’t your fault

While it’s easy to wag a finger at Americans for their lack of retirement savings, the reality is far more complicated than just bad spending habits or financial ignorance. Much of this mess stems from factors beyond individual control—an economic system engineered to encourage spending now and worrying about tomorrow later.

We live in a consumption-driven economy where corporate greed and political sleight of hand have shaped financial priorities. Companies have perfected the art of making sure we focus on immediate gratification, whether it’s the latest iPhone, a new streaming service, or, yes, the urge to DoorDash sushi at midnight. This “buy now, think later” culture has created an environment where retirement planning feels as thrilling as watching paint dry.

Even worse, political policies have often sided with corporations, favoring short-term profits over long-term security for the average citizen. The transition from pension plans to 401(k)s in the late 20th century is a perfect example. By passing the responsibility for retirement savings from employers to individuals, companies neatly sidestepped one of their largest financial obligations. Meanwhile, Wall Street gleefully swooped in to collect fees, leaving individuals with the stressful burden of navigating retirement planning solo.

And let’s be real: it’s hard to save for the future when you’re still figuring out how to pay for the present. Wages have remained stagnant while living costs have skyrocketed, making retirement savings more of a luxury than a necessity. As the saying goes, you can’t pour from an empty cup—and Americans’ cups are often bone-dry.

Then there’s hedonic adaptation, our natural tendency to get used to new luxuries and quickly want more. Remember when a cell phone was a luxury? Now, it’s basically oxygen. We used to be thrilled with basic cable; now, we can’t live without subscriptions to Netflix, Hulu, HBO Max, and Disney+. Each year, our definition of “normal” keeps upgrading—bigger homes, more innovative gadgets, and better shoes (because clearly, one needs 20 pairs even if they only wear five).

And let’s not overlook the impact of the COVID-19 pandemic. The stress cycles Americans have been stuck in since 2020 have only deepened the problem. Between job instability, economic uncertainty, and the pressure to stay connected in isolation, many turned to “comfort spending” to cope. A survey by Northwestern Mutual found that nearly a third of Americans reported splurging on non-essential items during the pandemic as a form of stress relief. That $15 daily latte might be a financial crime to future you, but to present you, it’s an act of self-care.

So, can we really blame Americans for choosing the here and now over some far-off, fuzzy concept of retirement? Not entirely. The truth is: the game is rigged. Between corporate manipulation, political policies, and human psychology, the system isn’t designed to help people save. It’s built to make us spend and spend again until one day, we wake up and wonder, “Wait, where did all my money go?”

To fix the retirement crisis, we need more than just scolding about saving more. We need a systemic overhaul—one that rebalances our economy to support long-term financial stability over short-term corporate greed. Until then, the average American is just trying to stay afloat in a sea of rising costs and shrinking paychecks.

So, meanwhile, . . .

Balancing living today with retiring tomorrow

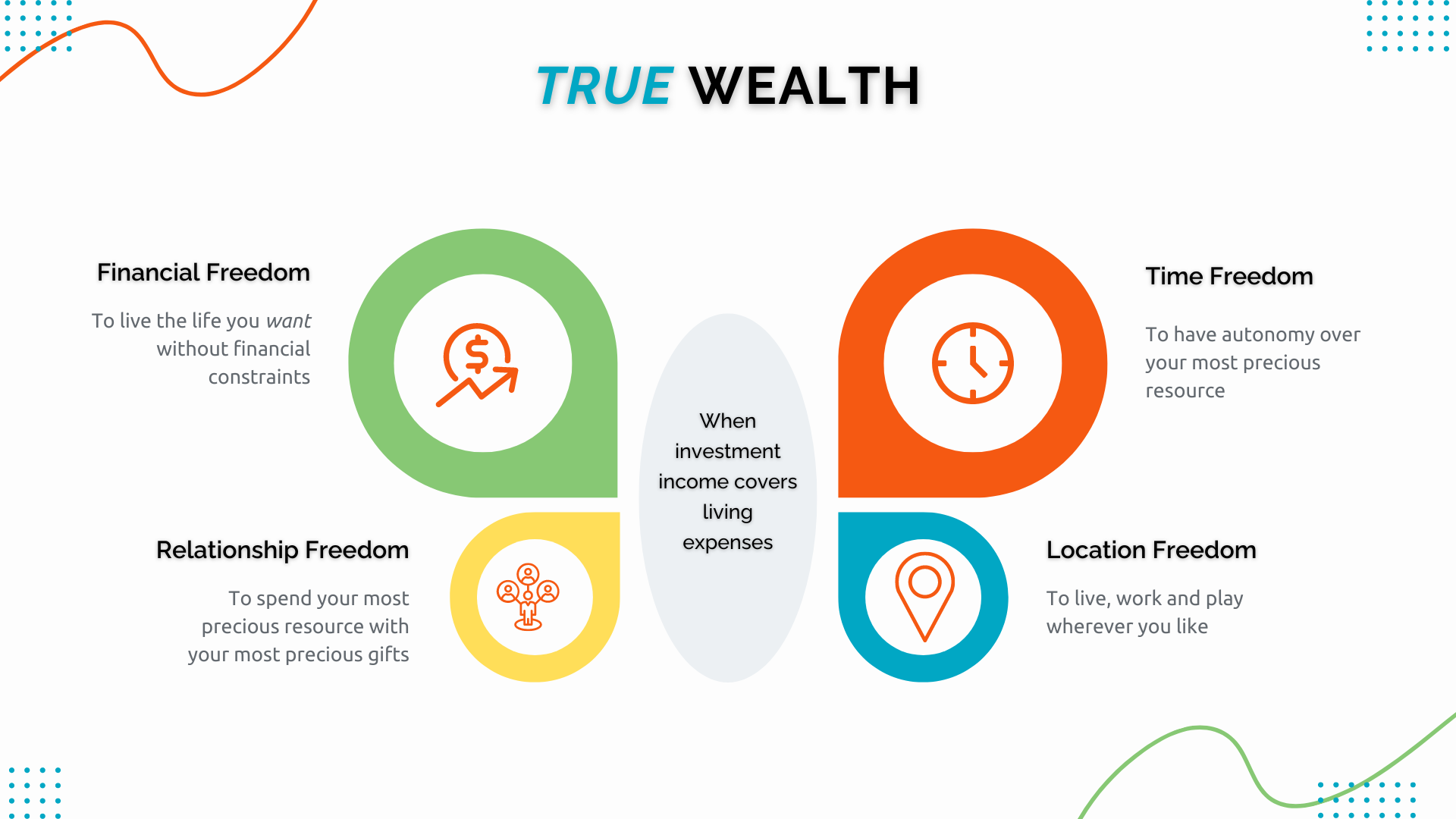

Remember, deep down inside, most of us want The Four Freedoms: 1) Financial, 2) Relationship, 3) Location, and 4) Time.

So what’s the solution? Americans must rethink the balance between enjoying the present and preparing for the future. Here are a few steps that can help:

- Automate Your Savings: Automate your savings by eliminating the need to think about saving. Setting up automatic contributions to your retirement account ensures you’re building toward the future, even when you’re focused on today.

- Reassess “Essentials”: Do you need 20 pairs of shoes? A quick audit of your spending habits may reveal opportunities to cut back on luxuries and redirect those funds toward your retirement goals.

- Start Small, Start Now: Even if you feel behind, it’s never too late to start saving. A little can grow into a lot with compound interest, especially if you begin early.

- Set Realistic Expectations: Retirement may not look like a never-ending vacation on a tropical island, but with careful planning, you can still maintain a comfortable lifestyle.

- Seek Professional Help: If you’re overwhelmed, financial advisors can help you create a personalized plan that fits your current situation and future goals.

At the end of the day, balancing today’s joys with tomorrow’s needs is a challenge many of us face. But with a little planning and discipline, it’s possible to have both—the fun and the future security.

Get some help with your retirement:

Read the full article here