Credit Sesame discusses how national finances represent average consumers but not all consumers.

American consumers have record debt. Rising delinquency rates indicate an increasingly hard time keeping up with the payments on that debt. But the economy has continued to grow and foreclosures and bankruptcies are nearly 40% below pre-pandemic levels. These would appear to be sharply contrasting views of the economy. Can both be correct?

Broad national financial statistics often fail to accurately represent the financial realities faced by many consumers. While national data provides an overview of the economic landscape, it can overlook the nuances and challenges experienced by individuals in their day-to-day lives. The fact is that national statistics cover such a large number of people that the financial challenges of many individual households are not reflected by those averages. Averages may look good even when a significant number of households have serious financial problems.

While those in financial trouble may be a minority of the population, the impact is significant enough to create problems for the economy overall.

Debt problems vary considerably state by state

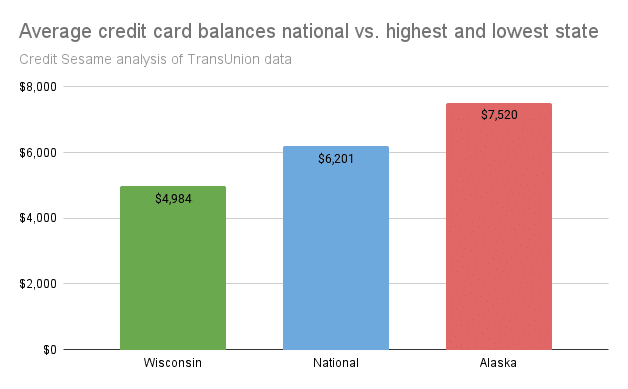

National averages are not good representations of the financial situation in all states. For example, Americans now owe a record amount of credit card debt. However, as the graph below shows, the picture is very different from the state with the most debt and the least debt and the national average. Credit Sesame took state-by-state data from the April 2024 TransUnion Credit Industry Snapshot and ranked the average balances from lowest to highest.

The national average credit card debt is $6,201. However, people in Wisconsin typically owe under $5,000, and people in Alaska typically owe more than $7,500. Alaskans have an average of $2,536 more credit card debt than Wisconsinans. The national average is unhelpful when considering these two states.

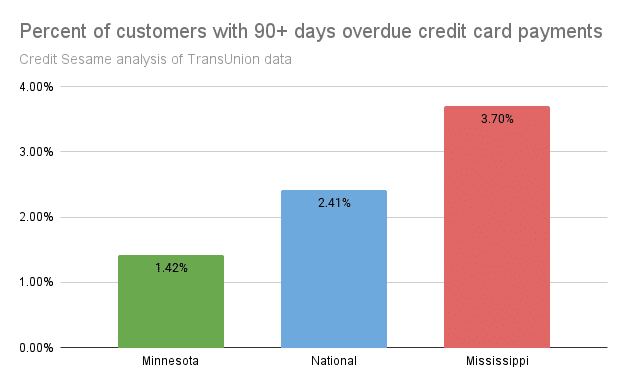

Another way credit conditions vary greatly by state is in the percentage of people who are seriously late on their credit card payments. This is shown by the graph below.

Nationally, 2.41% of credit card customers are 90 days or more late with their credit card payments. However, the average in Minnesota is 1.42%, and in Mississippi, it is 3.70%. People in Mississippi are more than two-and-a-half times more likely than people in Minnesota to be seriously late with their credit card payments. That represents a lot of people who see their credit scores plunge and their access to credit cut off.

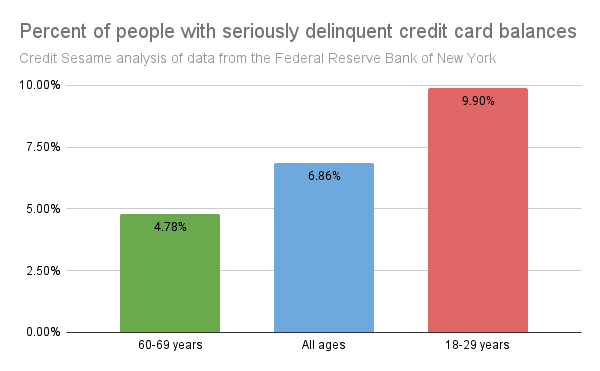

National finances do not represent all ages

Federal Reserve Bank of New York’s quarterly report on Household Debt and Credit indicates that age is a big factor in keeping up with credit card payments.

Nationally, 6.86% of credit card balances are seriously overdue. However, people aged 60-69 have under 5% delinquency, whereas nearly 10% of young adults 18-29 have seriously late payments on their credit card balances. Young adults are more than twice as likely to be overdue on their credit card payments, which could cause long-lasting credit problems.

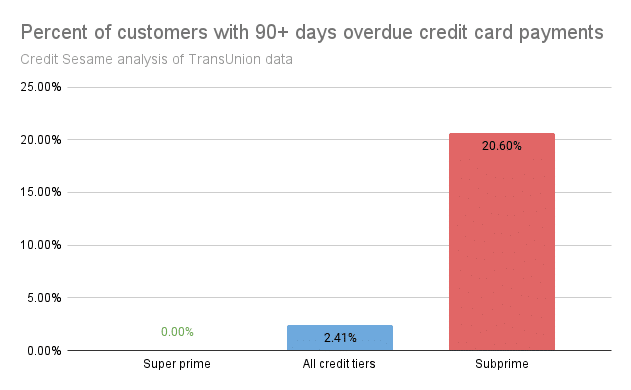

Consumers with credit problems are having serious trouble keeping up

People with low credit scores are more likely to be late with their payments than people with high scores.

Nationally, 2.41% of credit card accounts are 90+ days overdue. People with excellent credit scores of 781 to 850 (TransUnion “super prime”) have no 90+ day overdue payments. Subprime customers with scores of 600 or below have a 20.60% delinquency rate. That means slightly more than one in five subprime customers is 90 days or more overdue on their credit card payments.

The differences matter

The extreme ranges represented by economic data are important. The financial challenges experienced by people at the lower margins of the economy are very real.

The extremes of hardship represent a risk to the economy. When increasingly large numbers of people fail to repay their loans or credit card balances, it threatens the availability and cost of credit across the entire system. That’s why it’s important to look beyond the averages to understand the economy. Outlying data may be atypical, but the more extreme it is, the more reason to worry. As credit conditions deteriorate, lenders may become more and more picky about who they do business with. Even consumers who aren’t experiencing credit problems now would be wise to protect their credit history for the future.

If you enjoyed How national finances fail to represent reality you may like,

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.

Read the full article here