The failed assassination attempt on Donald Trump reminds us that more important than political bickering is the value of life. I hope there will be a coming together of both parties to help heal and strengthen the spirit of the American people. One inch to the right and Trump would probably be dead today.

After this incident, it is more than likely that Trump will become the 47th president of the United States. When you have the strength to get up after an assassination attempt with blood on your face and yell, “Fight! Fight! Fight!“, you galvanize the undecided and apathetic to vote for you.

Like Ruth Bader Ginsburg, President Joe Biden refuses to step down despite his diminished state, to the detriment of his party. Power is addictive. As a result, the probability of Trump becoming the next president has increased from 65% before the assassination attempt to 80%.

As this is a personal finance site, I thought it would be good to discuss what a Trump presidency could mean for your investments and finances overall. One of the keys as an investor is to think things through rationally, with the least amount of emotion possible.

What A Trump Presidency Means For Your Finances

In general, the Republican Party is for smaller government, lower taxes, and less regulation. The result of these policies could be an increased budget deficit. However, the general view from an investor’s perspective is that Republican policies are a net positive for your finances.

Here’s what you could see happen, although there are no guarantees:

1) A Potential Melt-Up in the Stock Market

Despite an extraordinary rise in the S&P 500 since October 2022, a Trump presidency will likely add fuel to the fire. As a result, if there’s a time to be greedier when others are already greedy, it could be now.

Investors will get excited about the continuation of the existing flat 21% federal corporate tax rate or a potential cut in the tax rate. Since January 1, 2018, the nominal federal corporate tax rate in the United States has been a flat 21% following the passage of the Tax Cuts and Jobs Act of 2017.

With a lower concern for higher tax rates, corporations will logically set aside less money for future tax hikes and spend more to grow their businesses, which includes hiring. With potentially lower corporate tax rates, corporations will be able to boost their profits, lowering their valuations, and increasing their dividend payouts.

The thing with investing is that potential positive catalysts don’t have to happen for stocks to go up. It is the hope and possibility of a potential catalyst that will help bid up stock prices.

As a result, despite high valuations in the S&P 500 and other stock indices, you probably want to hold on and continue dollar-cost averaging. If there is a 1% – 2% dip, you should probably buy. If there is a 10% or greater correction, you may want to back up the truck. This strategy shouldn’t differ from your general goal of investing for as long as possible in the market.

2) Tech Giants and Companies with Monopoly Power May Benefit More Under Trump

At the margin, President Biden is seen as a much tougher fighter against monopolies than Trump. In fact, battling monopolies is central to Biden’s economic strategy. As a result, companies facing antitrust suits like Amazon, Google, Microsoft, and Apple may see some relief under Trump, even though Trump also went after these companies.

Because we have not seen the federal government effectively break up tech companies’ monopoly power yet (just levy one-off fines), you probably want to just keep holding these big tech companies. Insurance companies like Humana and UnitedHealth Group, will likely also benefit.

We operate in a society where the rich and powerful continue to get richer and more powerful. Hence, you might as well keep owning shares in these dominant companies.

As soon as I saw Google roll out their artificial intelligence snippets in 2024, which plagiarize content creators without giving proper credit, I bought more Google stock. There’s also no way I can overcome OpenAI and Anthropic’s copying of my work, so I became a shareholder in both through a venture capital fund, which anyone can invest in too.

3) Real Estate Will Likely Strengthen Regardless of Trump

Trump has repeatedly admonished the Federal Reserve for its high interest rate policy. Trump is reportedly planning to override the Federal Reserve’s independence if he returns to the White House in 2025. The overriding of the Fed’s independence is unlikely to happen, but it’s nice rhetoric for votes from those hurting from high-interest debt.

Mortgage rates are already declining thanks to persistent disinflation since mid-2022. It is highly probable that the Fed will cut at least one time by the end of 2024 and multiple times by the end of 2025, regardless of who is President.

However, Trump built his fortune in commercial real estate. As a result, perhaps he will introduce more real estate friendly policies that will help the commercial real estate market recover.

Hold On Or Buy More Real Estate

With pent-up demand, a strong economy, and declining mortgage rates, there should be significant demand driving both residential and commercial real estate. As a result, I would not sell your rental properties or primary residence. Instead, I would hold on or buy more before a potential flood of demand.

I clearly remember the stressful times of bidding wars between 2000 – 2006, 2012 – 2018, 2020 and 2021, and the spring of 2024. Bidding wars are tough for buyers because there can only be one winner. I expect bidding wars to return in spring 2025 after a stronger-than-expected spring 2024.

If there is indeed a melt-up in the stock market, it will boost consumer wealth and help bring up real estate prices with it. The gap between the S&P 500 index and the S&P 500 real estate sector performance will likely narrow as a result.

I’m maxed out in terms of owning physical real estate after the purchase of our latest forever home in October 2023. Now I’m methodically dollar-cost averaging into private real estate through Fundrise. So far, I’ve invested $954,000 in private real estate since the end of 2016.

4) Trump may encourage you to work harder for longer

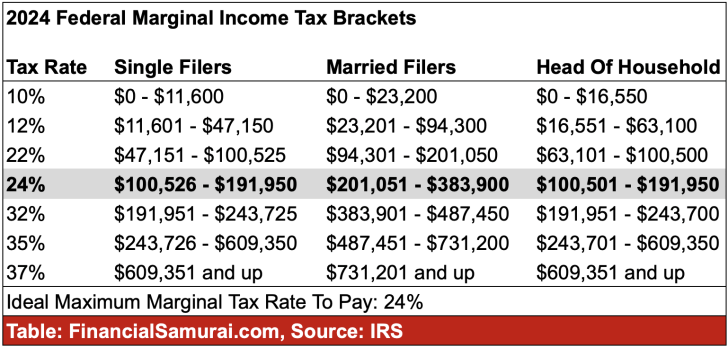

When income taxes are high, the rational economic move is to work less and retire earlier since you get to keep less of your money. Under a Trump presidency, the fear of income taxes increasing should diminish. The top federal income tax rate will likely remain at 37%, rather than rising to 39.6% as President Biden has been advocating since 2020.

To review, below are the current federal marginal income tax brackets for single, married, and head of household filers.

The ideal federal marginal income tax rate to pay is up to 24%. At this rate, you’re earning enough to live a good life, but you’re not paying so much in taxes that you are disincentivized to work. Jumping from a 24% to a 32% marginal income tax rate is significant, while offering not much more benefit for the additional income earned.

Americans who make six figures or have the potential to make six figures a year or more, thereby have the incentive to grind it out for four years under Trump. More workers working harder for longer equals greater output, which should like to greater profits, greater consumption, and a stronger economy.

Once again, those who believe higher income and capital gains taxes are coming will be wrong for at least another four years. As a result, the sense of urgency to contribute to a Roth IRA through normal or backdoor channels fades.

5) Speculative assets may also get a boost

Consistent with a potential melt-up in the S&P 500, there may be an even greater surge in the most volatile assets such as cryptocurrencies, public and private artificial intelligence companies, and venture capital overall.

Hence, you might consider allocating between 10% – 20% of your investable assets to more speculative investments in case they surge to nosebleed levels once again. With up to a 20% allocation, any outsized gains will significantly impact your overall investment returns. At the same time, if such investments correct by 50%, your finances won’t be devastated.

I’m dollar-cost averaging into an open-ended venture capital product that has a majority of its holdings in artificial intelligence. I’ve also committed capital to a couple of closed-end venture capital funds that will invest in AI. I don’t have the access or ability to pick AI winners, so I invest in various funds to hopefully find these unicorns.

6) Cash will likely be a significant underperformer

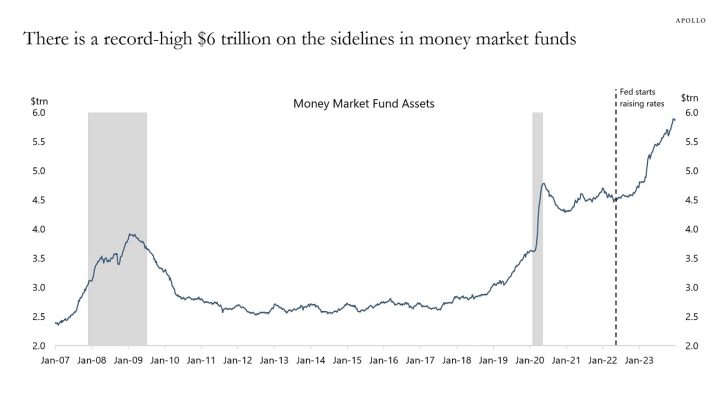

If the frenzy in risk assets continues under Trump and interest rates come down, then cash will be a significant underperformer. As a result, you want to put your cash to work, as holding too much cash could make you poorer over time.

There is supposedly a record ~$6 trillion in cash sitting on the sidelines. Stronger consumer and corporate balance sheets since the pandemic began is one of the main reasons why any downturn shouldn’t be as devastating as the one we experienced in 2008-2009.

If the amount of money market fund assets reverts to the level seen before the pandemic, there could be a $2.5 trillion unleashing of cash into risk assets. Even if the money market fund assets revert to the level right before the Fed started raising rates, we’re talking $1.5 trillion in cash looking to find a new home.

7) Buy American and protect America becomes popular again

During his first presidency, Trump was highly protectionist of U.S. companies. Trump imposed several tariffs to try and make U.S. companies more competitive and protect jobs.

After tariffs on Chinese goods jumped from 3 percent to 12 percent, China retaliated by raising tariffs as high as 25 percent on many U.S. goods, including agricultural products and food.

In general, trade wars are not good for economic growth as everything just gets more expensive for everyone. It’s like if one person stands up in the front row, everyone behind must stand up to see.

However, a Trump presidency could once again rejuvenate interest in investing in the heartland of America. More people who believe in Trump might be willing to move to Republican states to live and work. Surely, Trump will help those states that helped him return to power. Given this trend, you may want to focus on investing in heartland real estate and companies.

Everything Could Be Worse Than Expected Too

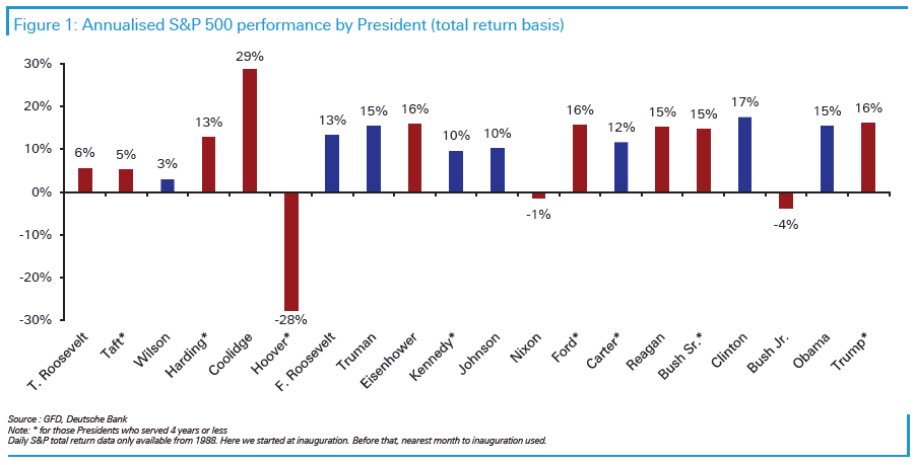

There are no certainties when it comes to investing. Despite Trump having an 80% probability of winning, Biden still has a 20% chance. Additionally, even with a 60% chance of a stock market melt-up if Trump wins, there’s still a 40% chance the stock market will either stagnate or decline.

The reality is that whether a Democrat or a Republican is in the White House matters less for your investments than you might think. Historically, the S&P 500 has performed well under both parties. Under Biden, the annualized return has also been over 10%.

Many variables influence the S&P 500’s performance, and the president is not a significant factor. It’s akin to the impact a CEO has on a large company’s performance, but even more diluted.

The CEO of one, a solopreneur, makes a huge difference to their company’s performance. On the other hand, if Tim Cook retired from Apple tomorrow, does it really matter? Plenty of lieutenants can fill his departure. Apple’s share price might actually go up, fueled by hopes of a more visionary and innovative CEO taking his place.

Strategically, to make a top 0.1% income, your goal should be to become a CEO of a large company! You don’t have to take any risks like entrepreneurs, yet you get paid obscene amounts of money for a job that plenty of people can do.

The President Only Plays A Small Part In Your Finances

The biggest factor in your ability to grow your wealth is YOU, not the president. You control your saving rate, work ethic, investment decisions, and career choices, not the president. Don’t rely on having the “right” president to help you achieve financial freedom.

Ultimately, every U.S. President is a power-hungry patriot who is trying to do what’s best for the most number of Americans. If the President does a poor job, thanks to our democracy, they will be voted out.

The failed assassination attempt on Trump is a good reminder to try to be good to others. Life is precious, yet fleeting. Try to understand other people’s points of view before attacking. Attempt to put yourself in another person’s shoes before judging. Connect through non-violence. We have more in common than we think.

My plan is to put my head down and do whatever it takes to take care of my family over the next four years. I’m grinding my way back to financial independence, with now slightly greater belief that I’ll get there by December 31, 2027. Along the way, I will try to help readers achieve financial freedom sooner, no matter their political affiliation.

Since 2009, I’ve found that people who are more financially secure are nicer and happier, and more good comes into the world as a result.

Reader Questions

What are the chances of Trump beating Biden to become the 47th President of the United States? If Trump wins, how do you anticipate his presidency influencing your investments and overall financial situation? Additionally, what other potential impacts could a Trump presidency have on your finances? Please share some recommendations and solutions if you are upset about Trump likely becoming the next president.

If you have children and debt, getting term life insurance is the responsible thing to do. You never know what might happen, please don’t risk being uninsured. Once my wife and I got matching 20-year term policies through Policygenius in 2022, we felt tremendous relief knowing that if something were to happen to us, financially, things would be okay for our kids.

Please note that I take action and invest in everything I believe in. I don’t always get things right, but I strive to learn from my mistakes and improve. I have too much skin in the game to not be thorough in my analysis. Invest only in what you understand and feel comfortable with. If you can’t explain to your friend or partner why you are investing, don’t invest. There are no guaranteed returns with risk assets. The dogged pursuit of financial independence is worth the sacrifice. Fight on!

Read the full article here